Free trial of Buy The Bull Market here:

https://newsletter.buythebullmarket.com/upgrade?offer_id=3f2ec885-4b68-4524-9c7b-2e16acc290e1

I’ve published my top stocks for 2024 here. Many of these have the potential to double (and you’ll be familiar with most of them) though they are, of course, not without risk.

But 2024 has started well and long may it continue.

In the last month, we’ve seen two big news events. Attacking the Houthi rebels and the approval of the Bitcoin ETF.

The SEC approving Bitcoin for an ETF is huge news.

Bitcoin was one of the best-performing assets of last year.

It’s one of the best-performing asset classes of this decade.

It was one of the best-performing asset classes of the last decade.

It’s easy to hate Bitcoin, but it’s easy to hate what isn’t easily understood.

Here’s the chart.

As crazy as the volatility is, Bitcoin gaining approval for ETFs now means more and more are going to take it seriously.

It means cash inflows, which in turn will drive the price. It’s not unrealistic to expect that Bitcoin will trade higher purely because of the money coming into the asset class.

But that’s not going to happen overnight, and many people will’ve bought the rumour and sold the news. So price now depends on how many people are selling the rumour and how many people are buying in due to this news.

Cash inflows can have a huge difference on asset classes. It’s no different to the crazily inflated prices in 2020 when scores of bored people at home suddenly joined trading apps and bought stocks. A cash inflow is the rising tide that lifts all boats. No different to quantitative easing.

I wouldn’t be surprised to see more crypto-focused businesses listed in London in the coming years to take advantage of Bitcoin and cryptocurrency’s more mature and growing profile.

But coming back to the Houthi rebels?

The UK is firing Sea Viper/Aster missiles which are estimated to cost around £1-£2m.

And the attack drones the Houthis are using are estimated to cost $20,000, or £15,690.

But if we say £20,000 to be conservative, that means the UK is using weaponry that is 50x as expensive as a minimum to combat drones.

Any of Britain’s enemies would surely be thinking that the more drones the Houthis fire, the quicker the costs will rack up to Britain, and therefore by providing weaponry it can hurt the Royal Navy in a financial war.

This is similar to how the Western world is using Ukraine as a proxy war against Russia. The West has delayed giving Ukraine the equipment it needs, because, in my opinion, a long war of attrition damages Russia (but comes at the expense of Ukraine).

In any case, this has the potential to escalate. But how much a driver it will be on markets I’m not sure, as interest rates falling has often meant that it’s game on again for stocks.

Finally, Ferrexpo has also introduced a dividend.

This is hugely significant and shows that the company clearly believes it is financially capable of maintaining this even though there is currently a war going on in its country of operations. My view: buy FXPO on any peace agreement/removal of uncertainty.

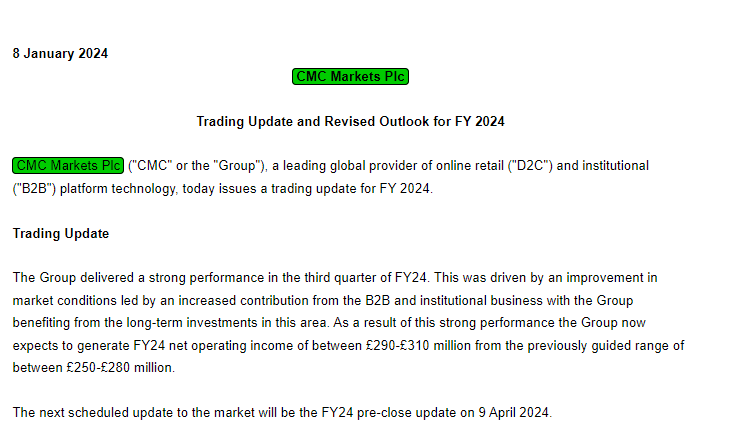

CMC Markets

CMC Markets is a spread bet and CFD provider. It competes with IG and Plus 500.

I’ve never met a CMC Markets or Plus 500 client in real life, but the business is doing better than expected as it released an ahead-of-expectations RNS earlier this week.

The stock started rallying in December and gapped up on the news. It was hard to do this trade in bigger size because it had rallied and so I didn’t want to be liquidity for people who were in the know.